Vietnamese real estate market is gradually recovering after a prolonged slowdown. While 2025 is widely seen as a transitional year, multiple indicators suggest that 2026 could mark a true breakout phase for Vietnam real estate, particularly for developers with strong legal foundations and project pipelines ready for handover.

Contents

One of the most critical developments is the government’s aggressive push to resolve legal bottlenecks. Authorities are currently reviewing and unlocking approximately 2,200 stalled real estate projects, covering 347,000 hectares with a total investment value estimated at USD 235 billion.

These initiatives are expected to unlock a significant volume of supply – particularly in commercial and social housing segments that have been constrained for years. NSI highlights that this legal clearance will not immediately flood the market but will gradually restore development pipelines, enabling developers to launch and deliver projects in phases from late 2025 through 2027.

In the first nine months of 2025 alone, both the number of licensed projects and newly launched products increased sharply compared to 2024. During Q3/2025, the Ministry of Construction approved 113 new commercial housing projects, while 79 projects met sales eligibility requirements, contributing approximately 32,000 units to future supply.

By the end of Q3/2025, total housing inventory – including apartments and landed houses – reached 18,650 units, marking a 37% quarter-on-quarter increase. Rather than signaling oversupply, NSI views this inventory as “stored value” – projects that are legally ready and positioned for delivery once demand fully recovers.

Market observers widely view this inventory accumulation as a necessary precondition for a strong 2026, as developers are expected to accelerate project handovers and revenue recognition across the Vietnam real estate market.

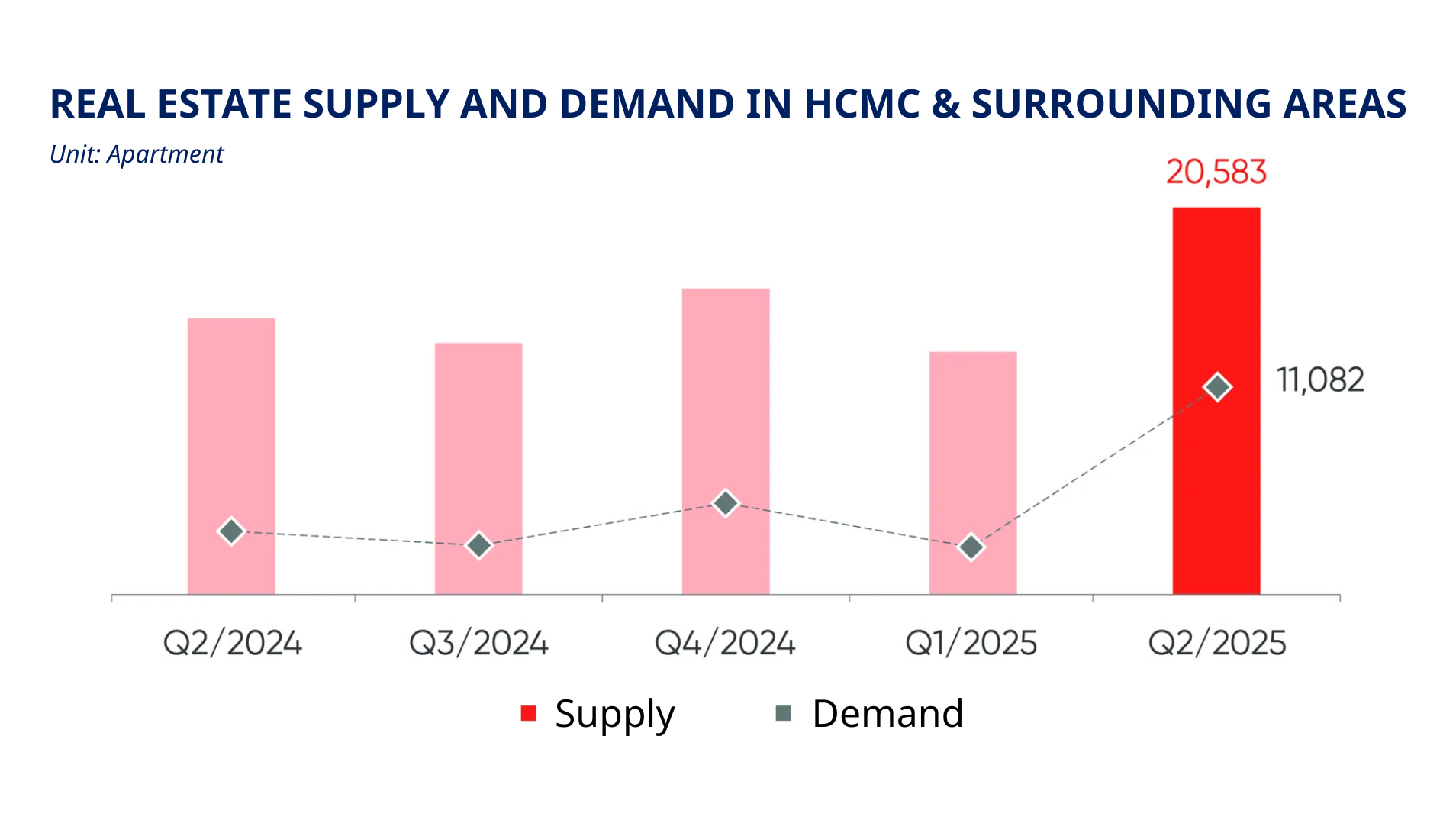

Despite increasing supply, total transaction volume in Q3/2025 declined to approximately 136,700 transactions, down 13% quarter-on-quarter, mainly due to a slowdown in land plot trading. In contrast, apartments and landed housing maintained more than 32,000 transactions, reflecting stable end-user demand.

Price trends remain firm. Apartment prices in Hanoi and Ho Chi Minh City continue to set new records, driven by rising construction costs and limited clean land availability. NSI notes that short-term price declines remain unlikely – particularly in central areas, Da Nang, and well-connected secondary cities – while government-led affordable housing programs will help stabilize long-term price growth.

New regulations, including Decree 192/2025/NĐ-CP, Resolution 155/2025/NĐ-CP, and Decree 230/2025/NĐ-CP, have streamlined approval procedures and allowed social housing developers to self-determine selling prices. These reforms significantly reduce administrative friction and shorten project timelines.

Public investment remains a decisive growth driver. As of the first nine months of 2025, public investment disbursement reached approximately VND 440 trillion, equivalent to 50% of the annual plan. Major infrastructure projects – such as Long Thanh International Airport, the North–South high-speed railway, and metro lines in Hanoi and HCMC are expected to reshape demand toward suburban and satellite markets, forming new real estate growth corridors.

:quality(75)/san_bay_long_thanh_o_dau_6_1ebf86c215.jpeg)

By the end of Q3/2025, outstanding real estate credit reached approximately VND 4.1 quadrillion, accounting for 22–23% of total bank credit. Credit for real estate business activities exceeded VND 1.81 quadrillion, up 10% compared to May 2025. Medium- and long-term interest rates remain relatively low, favoring legally sound projects.

Meanwhile, the corporate bond market has shown clear recovery signals. Real estate bond issuance during the first nine months of 2025 totaled VND 67,858 billion, up 21% year-on-year, helping developers regain access to long-term capital and restart delayed projects.

Vietnam’s large-scale urbanization is not a short-term cycle but a structural transformation driven by population growth, infrastructure expansion, and policy reform. In this new phase, effective investment strategies are shifting away from short-term speculation toward assets with sustainable fundamentals. For individual investors, this means prioritizing projects with clear master planning, complete legal status, and locations aligned with long-term urban development rather than chasing early-stage price momentum.

At the same time, the financial health and execution capacity of developers have become decisive factors. As capital flows normalize and legal bottlenecks ease, reputable developers with strong balance sheets and proven delivery records can better position their projects to benefit from the upcoming 2026–2027 supply cycle. Investing alongside infrastructure development – such as metro lines, ring roads, and regional connectivity projects – also increases the probability of stable value appreciation, especially in emerging urban zones.

Ultimately, Vietnam real estate is entering a phase where patience becomes a competitive advantage. Medium- to long-term holding strategies allow investors to benefit from project completion, infrastructure realization, and improving market sentiment. For individual investors seeking lower risk and sustainable returns, disciplined project selection and alignment with real housing demand will define success in the next growth cycle.

With a mission to support international investors in Vietnam, La Quinta provides full market insights, forecasts, and legal updates to help investors make informed, effective decisions in this fast-growing market.

More potential real estate in Ho Chi Minh City